The concepts related to these notes can easily be applied to other forms of notes payable. The agreement calls for Ng to make 3 equal annual payments of $6,245 at the end of the next 3 years, for a total payment of $18,935. Notes payable is a liability that results from purchases of goods and services or loans. Usually, any written instrument that includes interest is a form of long-term debt. The debit is to cash as the note payable was issued in respect of new borrowings. The first journal is to record the principal amount of the note payable.

AccountsBalance

Also, the process to issue a long-term note is more formal, and involves approval by the board of directors and the creation of legal documents that outline the rights and obligations of both parties. These include the interest rate, property pledged as security, payment terms, due dates, and any restrictive covenants. Restrictive covenants are any quantifiable measures that are given minimum threshold values that the borrower must maintain. Maintenance of certain ratio thresholds, such as the current ratio or debt to equity ratios, are all common measures identified in restrictive covenants. As the customers receive the cash, there is an increase in their assets, and hence they debit the account. At the same time, notes payment is a credit entry as they promise repayment, which is a liability.

Financial Accounting

This payable account would appear on the balance sheet under Current Liabilities. A short-term notes payable created by a purchase typicallyoccurs when a payment to a supplier does not occur within theestablished time frame. The supplier might require a new agreementthat converts the overdue accounts payable into a short-term notepayable (see Figure 12.13), with interest added. This gives the company moretime to make good on outstanding debt and gives the supplier anincentive for delaying payment. Also, the creation of the notepayable creates a stronger legal position for the owner of thenote, since the note is a negotiable legal instrument that can bemore easily enforced in court actions. The date of receiving the money is the date that the company commits to the legal obligation that it has to fulfill in the future.

Would you prefer to work with a financial professional remotely or in-person?

The sum of interest and principal which is the total payment is equal from year 1 to year 6. A group of information technology professionals provides one such loan calculator with definitions and additional information and tools to provide more information. Note that since the 12% is an annual rate (for 12 months), it must be pro- rated for the number of months or days (60/360 days or 2/12 months) in the term of the loan.

- These notes are negotiable instruments in the same way as cheques and bank drafts.

- As mentioned above, there are two payment patterns on the notes payable.

- The preceding illustration should not be used as a model for constructing a legal document; it is merely an abbreviated form to focus on the accounting issues.

- At the initial recognition, the notes are recorded at the face value minus any premium or discount or simply at its selling price.

Notes payable are liabilities and represent amounts owed by a business to a third party. What distinguishes a note payable from other liabilities is that it is issued as a promissory note. Notes payable are the portion of the current liability section on the company’s financial statements at the end of the specific period. An interest-bearing note is a promissory note with a stated interest rate on its face.

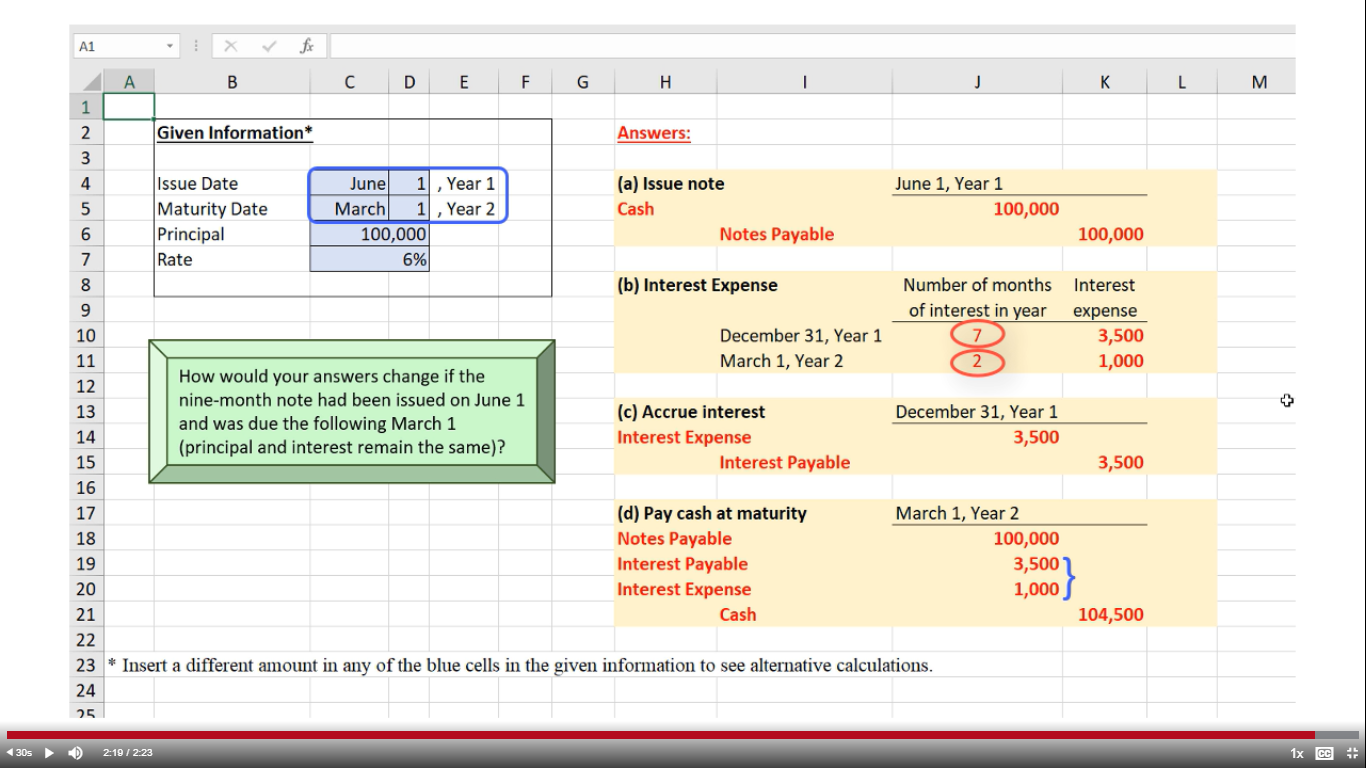

Taking out a loan directly from the bank can be done relatively easily, but there are fees for this (and interest rates). Issuing notes payable is not as easy, but it does give the organization some flexibility. For example, if the borrower needs more money than originally intended, they can issue multiple notes payable. The organization borrows money from the owner of the firm, and the borrower agrees to repay the amount borrowed plus interest at a specified date in the future. The adjusting journal entry in Case 1 is similar to the entries to accrue interest. Interest Expense is debited and Interest Payable is credited for three months of accrued interest.

Likewise, lenders record the business’s written promise to pay back funds in their notes receivable. Recording notes payable in their entirety is crucial for the fair and true representation of the financial statements. The notes payable of a company can also be added to project expenses when you’re budgeting for future periods. This establishes the importance of notes payable recording in financial statements.

The entry is for $150 because the amortization entry is for a 3-month period. After the entry on 31 December, the discount account has a balance of only $50. Thus, S. F. Giant receives only $5,000 instead of $5,200, the face value of the note. On November 1, 2018, National Company obtains a loan of $100,000 from City Bank by signing a $102,250, 3 month, zero-interest-bearing note.

When Sierra pays cash for the full amount due, including interest, on October 31, the following entry occurs. A troubled debt restructuring occurs if a lender grants concessions such as a reduced interest rate, an extended maturity date, or a reduction vehicle title, tax, insurance and registration costs by state for 2021 in the debts’ face amount. These can take the form of a settlement of the debt or a modification of the debt’s terms. Here are some examples with journal entries involving various face value, or stated rates, compared to market rates.

The company owes $40,951 after this payment, which is $50,000 – $9,049. In the following example, a company issues a 60-day, 12% discounted note for $1,000 to a bank on January 1. On June 1, Edmunds Co. receives a $30,000, three-year note from Virginia Simms Ltd. in exchange for some swamp land. The land has a historic cost of $5,000 but neither the market rate nor the fair value of the land can be determined.